[ad_1]

In the days before mobile internet spread across India, Byju Raveendran, an engineer and test preparation tutor from a coastal village in Kerala, could hold the attention of a stadium full of thousands of teenagers with the power of numbers. Or, at least, the magic numbers they would need to pass India’s competitive standardised engineering exams.

But despite running teaching events on a scale he would later describe as “almost like a maths concert”, Raveendran wanted a bigger audience. By 2015, he launched his own teaching app: Byju’s.

Today, the Bangalore-headquartered group offers smartphone, or tablet-based, learning to students from primary school age upwards, using graphics and cartoons to liven up video lessons. The company says it has 150mn-plus users, although less than 10 per cent are subscribers, who pay an average of Rs15,000 ($180) for an annual membership to the app. Parents can pay more for live lessons and personal attention from teachers.

“Back in the day in India, if a teacher had 1,000 students in a class it was a matter of pride,” says Pratheek Rao, a creative director who worked at Byju’s from February 2021 to earlier this year. “I think [Raveendran] wants to be that one professor who has taught all the students in this world.”

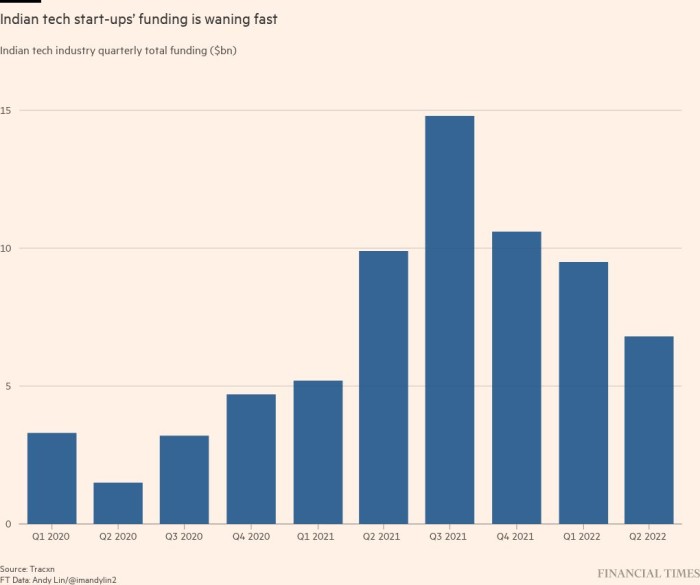

That vision, and an influx of investor funds that poured into Indian tech startups during the Covid-19 pandemic, vaulted the charismatic teacher to stardom and made him one of India’s richest people. Today, Byju’s is valued at $22bn, the most of any ed-tech start-up in the world. Its backers include the Chan Zuckerberg Initiative, set up by Facebook founder Mark Zuckerberg and his wife, Priscilla Chan, as well as China’s Tencent and the US hedge fund Tiger Global. In turn, Byju’s has acquired some 20 other companies worldwide.

When the government’s strict Covid lockdowns kept families at home in 2020, it seemed a surge in online learning would prove a breakout moment for ed-tech. So it was all the more surprising when an auditing and accounting wrangle delayed the filing of Byju’s mandatory 2021 results for a full 18 months. When the numbers finally did emerge in September, they showed flat revenue and ballooning losses equivalent to $560mn.

Scrutiny of the company during the long delay has brought questions over Byju’s accounting practices, exposed millions of dollars in expected investments that Byju’s now says it never received and uncovered accusations of mis-selling to parents. It has also shone a light on a sales culture described by employees as “toxic”.

Investors have expressed doubts about a strategy of rapid-fire deployment of funds to expand globally. The company’s valuation is now 10 times expected revenues for the year ending March 2023, according to Raveendran. Experts say the episode has cast doubt on the ed-tech sector’s ability to profit by converting casual users into paying subscribers.

One veteran of India’s start-up scene says the filing delay has “shaken the confidence of existing and new investors”. Raveendran “should not have . . . spoilt his reputation”, the veteran adds. “Hopefully he’s learnt his lesson.”

Others think Raveendran has been unfairly maligned. “When you’re this huge you get overwhelming opposition from all over,” says Jatin Kumar, chief executive of Indian real estate group ProperT. Cash burn and ambitious sales targets are problems faced by many fast-growing companies, he adds. “It has to be steered with utmost caution . . . otherwise it will fall like a house of cards.”

Raveendran himself seems uncowed by the allegations and blames losses on new accounting practices, which have reduced the amount of revenue that Byju’s can book upfront. “Even during tough times like these, in the last 12 months not a single investor has sold,” he says. “The world needs 10 more Byju’s.”

Pain points

Raveendran’s pitch to parents speaks to a deep-rooted anxiety among many families in India that the only way for their children to succeed is through gaining entry to a respected college or university and, from there, into a well-paying job.

The 41-year-old is not the first self-styled education guru to offer a leg-up in India’s fearsomely competitive school exams for disciplines such as engineering and medicine, seen as the gateway to affordable, quality public universities. Acceptance rates are low because demand for higher education far outstrips supply — the government’s foreign investment promotion arm estimates some 35,000 new colleges and 700 new universities are needed to keep up with demand.

In response, a thriving industry of exam coaches, tutors and cramming institutions has done good business for decades. Infinium Global Research, a Pune-based consultancy, expects India’s coaching classes industry to be worth $500mn this year. Not all play by the rules. Every exam season seems to bring new allegations of cheating by a coaching institute.

“The ‘Indian dream’ . . . will always revolve around education assuring a good share of customers’ wallet,” wrote analysts Pranav Bhavsar and Nitin Mangal last year. “Byju’s has been able to capitalise on this.”

Raveendran, the son of schoolteachers, says his entry into the industry was accidental. While working at a shipping company he took a standard entrance test for fun and aced it. He started teaching others how to take the exams, later setting up a test prep company with his wife, Divya Gokulnath. After securing their first outside investments in 2013, the couple decided to expand beyond university exam prep and into primary education.

Their model was more ambitious in scope than many of its predecessors: a learning app preloaded on to a tablet that would engage even young children, delivered by the best teaching talent anywhere in India and with personalised follow-up support.

Yet it tapped the same old anxieties. “We used to hit on those pain points: ‘Don’t you want to give your child a good education?’” says a former salesman who worked with Byju’s in 2018. “We were trained to say those things bluntly to the parents’ face.”

In product demonstrations at family homes, salespeople tested children with tough questions. “You have to push the students and parents by demeaning them, telling them, ‘You are not good in your studies’,” says a second former salesman. Raveendran says Byju’s training material does not contain “anything like this”.

In 2015, with internet access pushing into every corner of the country, the potential to investors was obvious. India’s education market is expected to be worth $225bn by 2025, comprising the world’s biggest cohort of people aged under 24. Some 37 per cent of more than 250mn students attend fee-paying private schools — and aspirational parents spend whatever they can on extra tuition. Within three years, Raveendran had attracted more than $180mn in investment.

At the same time, the new prime minister, Narendra Modi, had promised to create 250mn jobs as part of an appeal to young people trying to navigate a difficult job market with changing skills requirements. Thousands of IT and engineering graduates were drawn to tech start-ups, flush with foreign money. Many were offering better salaries than even India’s IT giants such as Infosys and Tata Consultancy Services. The stage seemed set for exponential growth.

Forcing the moment

“Hello children,” said Raveendran to the camera. “We are all up against a crisis.” Covid-19 was surging across India, closing schools and affecting some 286mn children. In the 35-second video, which has been watched 12mn times on YouTube, he pledged to help kids keep learning, offering free live lessons.

As central banks the world over brought down interest rates, India’s tech start-ups were swimming in cheap money. Byju’s was no exception. Between March 2020 and the end of 2021, the company raised more than $2.5bn from investors, according to data provider Tracxn.

Byju’s put that money to work buying up foreign and domestic companies and gathering them under its brand. Its acquisitions in the US, in particular, were highly unusual for an Indian start-up, given the generally higher valuations of American companies: it suggested a new level of confidence among India’s tech outfits.

But Byju’s growth engine was its salespeople. Interviews with a dozen former and current employees, who worked across the company over the past four years, described a target-oriented organisation that was generous with incentives (in 2019, it flew high-performing employees to the UK for an international cricket match) but tough on workers who fell behind.

By 2018, the sales floor at Byju’s Bangalore headquarters was “like a college frat party, where you’re getting paid”, says one saleswoman, recruited from her college campus. “The culture was very weird: they openly swear,” she says, adding that she saw managers “shout” and “scream” at workers and colleagues cry in the office. Two salespeople who worked for Byju’s in Kolkata say their office floor was nicknamed “Wolf of Wall Street”.

“I’ve sat [at work from] 8am in the morning to 1am,” says Rao, the creative. “I have hired people who wanted to quit within two to three months . . . this is not for the weak hearted.”

Byju’s contests such descriptions and says it is “mindful of employee wellbeing” and has low attrition rates that indicate it is a workplace with a “culture of guidance and nurturing”. Raveendran acknowledges “higher pressure” in sales due to targets, “but if we come across wrongdoing we do take strict action”, he says.

In a 2019 interview, Raveendran told the Financial Times that “almost all” of his first 300 employees had been alumni of the Byju’s student base, providing him with an edge over his competitors and “a large student following; a fan following. I was able to attract the best talent to come back and join me.”

Rao says he admired Byju’s drive and vision. “I told myself if I want to survive in this company . . . I have to match the pace of the organisation.” With the start-up growing at breakneck speed, junior sales workers quickly jumped into managerial roles. But without enough wealthy parents to sell to, competition was fierce.

Sometimes, salespeople admitted, their tactics crossed ethical boundaries such as not telling parents about a 15-day refund policy. “Due to the pressure of losing your job, sometimes the salesperson has to do whatever you have to do for sales,” says one, who is still working at Byju’s.

Many parents went into debt to pay. Some used credit cards, but others took out loans with fintech companies, fellow risers in India’s start-up scene that were often willing to take on risky credit traditional banks might avoid.

In a statement, early Byju’s financing partner Zest Money say they pulled back from the relationship “owing to the mis-selling of their products to customers. This impacted the overall customer experience on both platforms.” Raveendran says Zest Money was “never a big partner”. He says a central team is now auditing every sale: “I won’t say zero but its almost impossible for people to do mis-selling today.”

Flatlining

One father in New Delhi, who asked not to be named because he is still in debt, signed his nine-year-old son up in 2019 after Byju’s salespeople “regularly and persistently” came to his door. He took a loan worth Rs34,000 (about $420) to pay for a three-year package.

The office assistant says he wanted “to do all I could to make sure my son would grow up to [ . . . ] not have to live the hard life like us, for lack of good education.” He was already spending more than one-third of his Rs12,000 ($150) monthly income on fees at a private school. Byju’s payments added Rs2,833 more. But the pandemic made this precarious arrangement untenable.

Even as online learning seemed the cure for school closures, many parents were squeezed as businesses fired workers or stopped their salaries. In late 2021, as complaints about Byju’s began to proliferate, the BBC published a bruising investigation into its sales practices. Byju’s rejected the allegations, but its image was damaged. Raveendran says Byju’s now has a non-profit organisation that helps parents struggling to pay with free tuition.

“The three things — mis-selling, aggressive sales and consumer financing — these are one-off incidents and anecdotal things,” he says. He cites a Bain and Company report, which judged evidence of Byju’s mis-selling to be “limited” and the risks posed by consumer financing to be low for investors.

International Finance Corporation, a sister investor of the World Bank that bought a $15mn stake in Byju’s in 2016, says it was “aware of media reports pertaining to aggressive sales tactics in the [edtech] sector and has advocated for solutions”. It says Byju’s had “taken measures to prevent such incidents from taking place”. IFC was the only one of the 15 Byju’s investors approached by the FT that agreed to comment.

When Byju’s auditor, Deloitte, signed off in late August, the edtech revealed feeble-looking results caused by a major change in accounting policies — at Deloitte’s advice. Byju’s had previously booked the majority of its revenues from selling preloaded tablets upfront, even though parents were buying multiyear plans. Yet, during the pandemic, free live video lessons were also used by existing customers. Classified as a service, auditors advised that these live-lesson revenues should instead be accounted for over time.

Deloitte also advised Byju’s that revenues from packages sold to customers on credit, a practice begun during Covid, should be booked only when collected in full. All in all, Raveendran says, the accounting changes deferred roughly Rs20bn out of Rs45bn revenues. Losses at Whitehat Jr, an online coding school Byju’s acquired in August 2020, weighed on the group.

Ferocious marketing also drove steep losses of Rs45bn ($555mn), with swelling expenses of about three times revenues. Nirgunan Tiruchelvam, head of consumer sector research at analytics group Tellimer, says more than 90 per cent of costs came from promotional activities such as sponsoring the Indian cricket team and other celebrity endorsements as well as employee benefits. “Investors need to figure out if Byju’s can turn off the marketing expense tap and go back to [growth] by word of mouth,” he says.

There was also some bad news on funding. Two US-based venture capitalists, Oxshott Capital and Sumeru Ventures, failed to deliver investments pledged over the past year worth about $250mn. Neither responded to requests for comment.

Byju’s is now looking ahead to a post-pandemic world. The founder, who once said “we have killed our offline business model”, is introducing a hybrid through opening tuition centres and a newly acquired coaching college, Aakash.

Yet if losses by other global edtech companies are any indicator, the next few years could be tough. Three US online education start-ups, Coursera, Udemy and Chegg, have about $400mn to $600mn in cumulative losses, says technology consultant Jeffrey Lee Funk. “I imagine the financial performance of these start-ups . . . will worsen as schools continue to open. It is likely that the same dynamic is operating with Byju’s,” he says. Byju’s says its revenues are rising strongly.

Raveendran has already moved on. He concedes that “investors and lenders were anxious” about the audit delay, but adds: “everything which auditors do is fair . . . short-term you might think, OK FY21 is a bad year from a reporting point [of view] but who cares right? We are thinking next 20 years.”

Source link