[ad_1]

maybefalse/iStock Unreleased via Getty Images

For a company like Alibaba Group Holding Limited (NYSE:BABA) with sentiment at all time lows, the company’s recent release 4Q22 results was a positive surprise for investors. I looked into the recent quarter and was pleasantly surprised that there were signs of improvement and that the worst is likely over for Alibaba.

Investment thesis

I have written two deep dive articles into Alibaba that you can read further to learn more about the business as well as the regulatory risks of the company. My investment thesis remains as I continue to see Alibaba as currently one of the better risk/reward opportunities out there due to the following factors:

1. China commerce: One of the most valuable assets Alibaba has is its huge consumer base of 1 billion users and spends $1,300 annually, which can bring about further monetization or help scale its other newer platforms.

2. International commerce: This business is a low hanging fruit for Alibaba as it has a replicable strategy and strong moat, as well as logistics capabilities to compete with international e-commerce brands in international markets.

3. Cloud: Alibaba will likely remain the leader in a fast growing cloud market in China and continue to look out for international markets to grow in. Furthermore, its in-house production of chips and development of OS could bring about further cost efficiencies and better products while reducing reliance on third party suppliers.

4. Investing for growth in the future: Alibaba is reinvesting its incremental profits into its strategic businesses which, in my view, is necessary to ensure Alibaba is able to compete and win competitors. Also, Alibaba is continuing its mergers and acquisitions strategy to acquire new businesses to capture future opportunities or bring value to existing businesses.

Cloud computing achieves scale and positive adjusted EBITDA margins

For the cloud computing segment, it reported revenues of Rmb19 billion in 4Q22, which representing 12% growth year on year. This was compared to the prior quarter’s growth of 20% year-on-year and prior year’s growth of 38% year-on-year. The slowdown is due to weakness in certain sectors, slowing economic activities, and the company’s strategic focus on higher quality revenues.

In particular, the weakness came from the internet industries like online education and entertainment. According to management, the cloud computing revenue growth would have been 15% year-on-year if the revenues from its top customer in the internet industry, Bytedance were excluded. According to management, Bytedance apparently stopped using Alibaba’s overseas cloud services for its international business due to requirements that are non-product related.

As a result of weakness in the internet sector, the revenue contribution from non-internet industries increased to 52% as several sectors like telecommunications, retailing and financials reported strong growth to offset the weakness in the internet industry.

On the margins front, the cloud computing segment posted positive 1% adjusted EBITDA margins in 4Q22, compared to -2% adjusted EBITDA margins one year ago. This was attributable to the gradual improvement in economies of scale for the business, as well as better loss control for Dingtalk. Management also expects that margins for the cloud computing business to continue to improve in FY2023 as top line growth continues. In my view, the margins profile of Alibaba’s cloud computing segment is at a pivotal moment for the business as it transitions towards positive adjusted EBITDA margins with improving economies of scale.

I think that is is also encouraging to see that management continues to see the long term potential in the cloud industry and Alibaba’s cloud segment despite the near term blip. Management believes that the cloud industry can grow 2 to 3 times in the long run to reach Rmb1 trillion in the next few years. This comes as the cloud plays a key role for the development of the economy and for digital transformation. With that, the focus for Alibaba on the cloud computing sector is crucial, and management believe that Alibaba needs to cater to the differing needs of different sectors to be able to leverage on this huge opportunity in the long run. In my view, the other positive is that this will continue to drive top line growth and with the cloud revenues of the entire company already exceeding Rmb100 billion in the last fiscal year, this translates to huge economies of scale and potential for cost reduction and efficiency improvement that will further drive upside to cloud computing margins in the near term.

China Commerce

Revenues from the China Commerce segment grew 7% year on year to Rmb 136 billion. There was a low teens year on year decline in GMV in April and management sees that there are signs of improvement in May. The total FY2022 GMV in China Commerce grew by 2% year on year.

Alibaba continued to grow on the user front. China commerce Annual Active Consumers (AAC) reached 903million, up 21 million users from the previous quarter and up 89 million users from a year ago. Notably, of these increases, 70% are from less-developed areas. This is in-line with Alibaba’s push towards rural and less developed customers to grow its customer base.

Specifically, we are seeing growth in Taobao Deals and Taocaicai. Taobao Deals AACs grew to more than 300 million, adding 20 million users in the quarter while paid orders on Taobao Deals grew 35% year on year in the current quarter. In addition, Taocaicai, Alibaba’s community market place catered to lower tier cities and rural areas continued to grow AACs to more than 90 million and more than 50% of these were first time fresh produce buyers on Alibaba. Also, Taocaicai GMV continued to expand in the last quarter due to improving average order values.

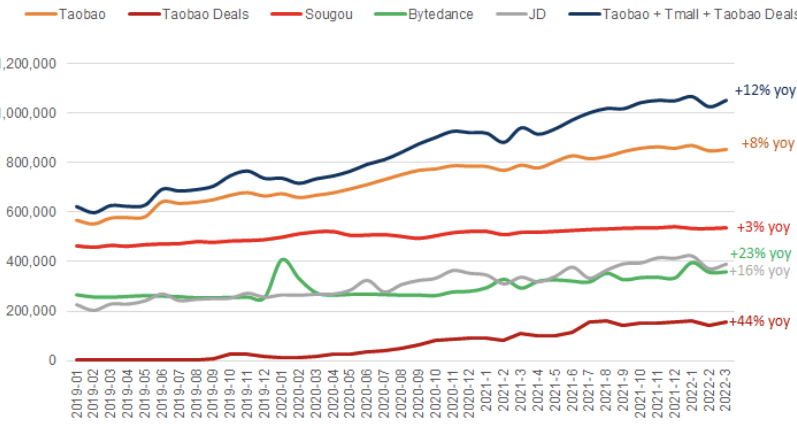

Alibaba recorded robust user growth compared to peers (QuestMobile; Goldman)

While there were low single-digit declines in Taobao and Small online physical goods GMV, the customer management revenues (CMR) remained stable year on year. This was due to some offset by positive growth in advertising revenues.

EBITDA declined Rmb 7 billion to Rmb 32 billion, representing an EBITDA margin of 23%. This decline in EBITDA margins was due to the drag from Taocaicai and Taobao Deals as management invests in these relatively higher growth and newer businesses. In addition, Sun Art reported a Rmb 1.4 billion loss, most of it due to an asset impairment provision.

Management remains committed to improving efficiency and narrowing losses for Taobao Deals. Furthermore, management has been more disciplined in investment pace for Taocaicai to reduce its impact on margins to the group. It has done so by choosing certain target cities where it aims to improve order density and thus focus establishing regional warehouses and infrastructure in these cities. Thus, the focus will be more on high quality growth for the Taocaicai business.

In addition, in my view, the combined losses from both Taobao Deals and Taocaicai has likely peaked in December 2021 and saw sequential declines in losses in the current quarter. I think we will continue to expect the combined losses to decline as management continued to focus on higher quality growth for China commerce segment.

International Commerce

Revenues from international commerce grew by 7% year on year as AACs grew 4 million compared to the prior quarter, and 64 million when compared to the prior year. There was a growth of 32% and 48% year on year respectively for Lazada and Trendyol while AliExpress saw a decline in order volume. This was due to the changes in EU’s VAT rules and supply chain/logistics disruptions due to Russia-Ukraine conflict, as highlighted by management. International commerce segment’s adjusted EBITDA margin remained stable at -18% as the company continues to spend on marketing and promotions to increase user engagement and acquisition.

International commerce remains to be one of Alibaba’s key growth drivers to tap on less mature e-commerce markets outside of China. While there could be near term competition from other e-commerce companies like Amazon (AMZN) and Shopee, which is owned by Sea Limited (SE), Alibaba’s international commerce can still ride the wave of increasing e-commerce penetration in these markets and post higher long term average growth rates than in the mature China Commerce segment.

Local Consumer Services

As for the local consumer services segment, revenues grew to Rmb 10 billion, up 29% year on year. Ele.me, Alibaba’s online food delivery platform, continued to show improvement in unit economics and is reaching near break even due to improvements in the delivery cost per order as well as the company reducing spend on user acquisitions.

As Ele.me continues to scale, its unit economics improvement as well as the cost reductions made by management will continue to contribute to bottom line growth for the Group.

Stringent cost control and improving regulatory environment

Management continues to be committed to add value by assessing the areas of its business where there can be further improvement in efficiencies and to reduce costs to make the entire cost structure of the business more nimble and lean. Some of these control in costs includes stringent control over sales and marketing expenses. This, in my view, is positive for Alibaba as the near term may prove challenging with top line slowing, and management’s efforts to provide long term shareholder value through cost efficiencies will be appreciated by the market.

The regulatory landscape also seems to be improving, adding to the signs that the worst could be over for Alibaba. In the recent State Council meeting, the government is rolling out supportive measures, some of which are beneficial to Alibaba’s business, including stimulating consumption and the commitment to the recovery of supply chains. Also, management commented that the government shared a clear message to the market to encourage the healthy development of platform economies and that management is fully compliant with all the regulatory requirements and continues to watch for any new development in policies on the anti-trust front. I think this shows that the government is sending a message that it will not clamp down too much on platform companies, but rather continues to see the benefits of the healthy development of platform companies for the economy.

Valuation

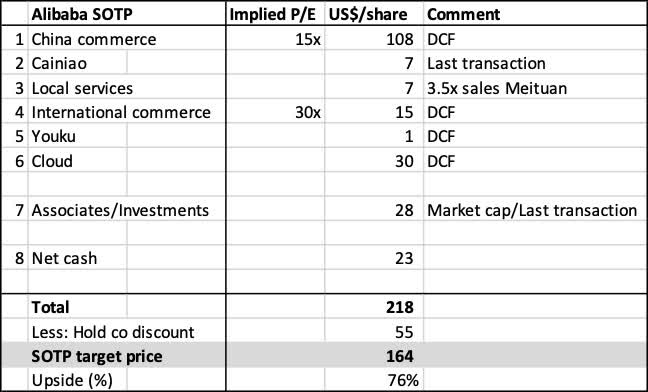

I have previously shared my financial model for Alibaba and derived a target price based on its sum of the parts valuation. I forecasted the financials and used a DCF model for most of its businesses except Cainiao, local services and its associates/investments since these businesses are mostly either private or have limited public information. I used rather conservative forecasts, in my view and also applied a holding company discount of 25%, with other assumptions listed in the table below. Based on the SOTP valuation, I have derived a target price of $164 for Alibaba, representing an upside potential of 76% from current levels.

Alibaba target price based on SOTP (Author generated)

Based on relative valuation, Alibaba now trades at 12x and 9x 2023F and 2024F P/E respectively, while average earnings growth over the 2-year period is expected to be 15%, implying a PEG of 0.8x.

Risks

Competition

While Alibaba might be the largest player in China, there are risks that competition could threaten Alibaba’s market share in both China and in overseas markets. In China, it has to compete against prominent rivals like JD.com (JD) and Pinduoduo (PDD) in a rather mature e-commerce market. As for its international commerce segment, they face competition from international players like Amazon and Shopee, as highlighted earlier. Competitive pressure from both local and international players could slow GMV and user growth for Alibaba compared to expectations.

Regulatory and political risks

Alibaba is one of the worst hit companies hit by the regulatory crackdown due to the saga with Jack Ma and the CCP, with the halt of the Ant Financial IPO, one of the first and biggest blows to the company. However, I am of the view that we have seen the worst of the regulatory crackdown and the government is signalling easing of regulatory pressures, which I think are necessary for the government to improve its economy amidst its zero-covid policy. As such, the worst is likely over for Alibaba as most of the regulatory pressures have eased and we could start seeing better times for the company.

Execution in investments

Alibaba management has renewed focus on investing in key strategic areas in its business as mentioned earlier. However, this will come down to execution as Alibaba seeks to gain share in these areas. If execution were to be weak, ideal results of the heavy investments may not materialize.

Cloud risks

There is risk that Alibaba’s cloud revenue growth could slow down given that there is competition from Huawei, Tencent and China Telecom. If Alibaba is unable to maintain market leadership in cloud, this could affect economies of scale effects that it currently enjoys.

Conclusion

I think this presents one of the best buying opportunities for Alibaba as the worst is likely over for the company. Looking beyond 2023F earnings, the business is expected to continue to grow in the 20% to 30% range and the current valuation simply just does not price in this long term potential. I think we could continue to see positive surprises for Alibaba in the next few quarters as it surpasses the very low expectations set by the market. My target price for Alibaba based on a SOTP valuation model is $164, implying 76% upside potential from current levels.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Source link